NEWSLETTER / SYSTEMS DRIVEN WEEKLY

The Personal Finance System for Entrepreneurs

How I applied Profit First to my own life so that a big exit would be gravy - and no exit still leaves me standing.

When it comes to personal finance, being an entrepreneur is disorienting.

Some days I feel like I'm on the road to being extravagantly wealthy, and other days I feel like I should be job searching.

But every day I have three kids, a mortgage, groceries, and a need to plan for my family's future.

So I built a system to help me manage this, paired with the following mindset:

Operate as if you're a boring W2 employee and your income will never increase. Give, save, and invest like everyone else.

My hope, of course, is for my income to grow exponentially. And perhaps I'll even have a big exit at the end that can fund my retirement. But since neither of those is guaranteed, I've got to find a way to be faithfully consistent with my finances now.

For this, I didn't turn to Dave Ramsey, but to Mike Michalowicz, author of the business book “Profit First.”

Giving and Investing Is a Decision, Not an Occurrence

Mike's thesis is simple: profit is not something that happens. It's a decision.

Most businesses (and families) run “Sales − Expenses = Profit,” which means profit is whatever accidentally survives after everyone else gets paid. And accidents are unreliable, so most businesses never see any.

Michalowicz flips it:

You take the profit off the top, first, on purpose - and you force the business to run on whatever's left.

The insight is that this isn't just true of profit. It's true of everything that matters and never feels urgent. Saving is a decision, not an occurrence. Investing is a decision. Giving is a decision. None of them will ever happen reliably if they're the leftovers, because there are never any leftovers.

So I stopped leaving them to chance. I decided - from the first dollar that comes in - exactly where the money goes. And what I have to spend is simply whatever remains after those decisions are already made.

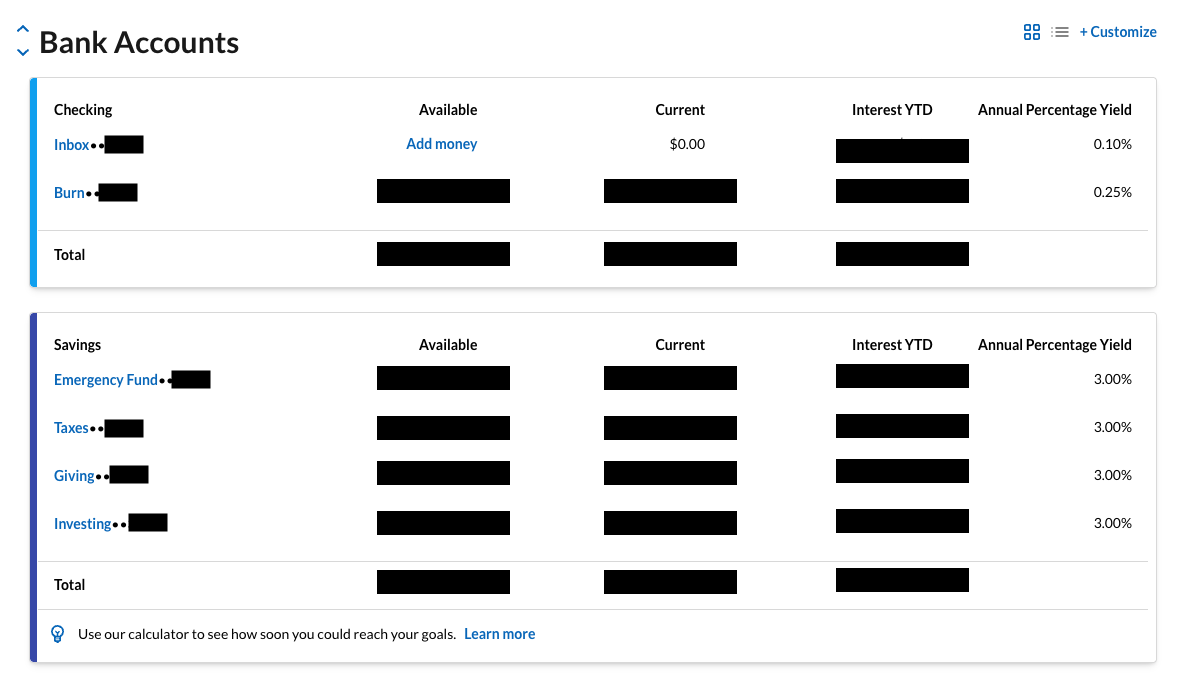

I Built It With Actual Bank Accounts

This isn't a spreadsheet exercise or a mindset. I did it the most literal way possible: I opened separate bank accounts, one for each decision. This is what Mike advises for your business.

In fact, Mike is so hardcore about it that he advises your “profit” account be at a small, physical bank that you have to drive to in order to make withdrawals. I don't go that far, but I do have separate accounts.

Here's how the money actually moves:

- Inbox (checking). This is where every dollar of income lands first - my business draw, my wife's paycheck. Nothing lives here. It's a lobby, not a home. Notice it sits at $0.

- Taxes (savings). Swept off the top the moment income arrives. As a founder taking a pre-tax draw, this is the account that wrecks people who skip it. I never touch it - it was never my money.

- Giving (savings). Our faith calls us to generosity, and I refuse to let that be a leftover. It gets swept first, right alongside taxes.

- Investing (savings). Off the top, before I ever feel “rich enough” to invest. This is the account that quietly makes the exit optional.

- Emergency Fund (savings). I maintain 10 months of living expenses, in cash. Entrepreneurship is risky - but not for me. This balance NEVER dips. And if it ever did, I'd fill it back up before I put a dollar anywhere else. Keeps me hard to kill.

- Burn (checking). Whatever's left after every decision above is already made. This is what we live on. Mortgage, groceries, kids, travel, the fun stuff.

The percentages are the engine. I don't budget fixed dollar amounts - I split by percentage, which matters enormously when your income is lumpy. A big month and a lean month get divided the exact same way, so the system scales itself instead of breaking every time the number changes.

But the real magic is the physical separation. The taxes, giving, and investing money leaves my checking accounts and goes somewhere I don't see day to day. What's left in Burn is the truth: that's what we have. There's no “well, I could dip into savings,” because savings was never sitting in front of me to dip into.

KEY INSIGHT

That's what I mean when I say by design, not willpower. I didn't become more disciplined. I removed the moment where discipline was required.

What If My Income Suddenly Doubled?

Legitimately, this has happened to me more than once. The plan: keep the “burn” amount the same and increase all the other categories - giving, investing, taxes.

My checking will never see the increase, which keeps lifestyle creep manageable.

Build Your Version This Week

You don't need my exact accounts or my percentages. You need the shape:

- Decide your top-line splits. Choose what comes off the top before spending - giving, taxes, investing, emergency fund - as percentages, not dollars. A good starting point: Giving 10% · Taxes 15% · Investing 15% · Burn 60%.

- Open the accounts and only deposit into “Inbox.” All my money lands in Inbox, and once a month I do the math and make the transfers.

- When investing and giving accumulate, distribute them. Confession: I don't have my giving or investing automated. About twice a year I invest or give in large chunks. Personally, I feel more connected to what I'm giving to and investing in this way.

Lastly, one benefit of running like this: even if you fail to keep track of your budget, you can look at your bank accounts and know exactly how much you have to spend - and be confident that you're saving for taxes, giving, and investing.

Hustle doesn't compound. Systems do. This is what that looks like when you point it at your own money.

P.S. I've hooked Claude up to Monarch Money, and it sends me a daily text with my budget plus a monthly email breaking down all my finances - which has been its own unlock. Reply if you have questions about that!